Why Credit Card Credit Lines Are Reduced After Inactivity

Overview

If you’ve ever noticed a sudden reduction in your credit card’s credit line, especially after a period of not using it, you’re not alone. Many cardholders find themselves facing this situation, often leaving them wondering why it happens. Understanding the reasons behind credit card credit line reductions due to inactivity is essential for managing your financial health. In this article by Academic Block, we will explore why credit card issuers reduce credit limits after periods of inactivity, how it affects your credit score, and what you can do to prevent this from happening.

What Is a Credit Line?

Before diving into the reasons behind credit line reductions, let’s first define what a credit line is. A credit line is the maximum amount of credit that a financial institution extends to you through your credit card. This limit is based on several factors, including your creditworthiness, income, and overall financial situation. Your credit card issuer may adjust this limit as needed based on your spending habits and how well you manage your payments.

Why Do Credit Card Issuers Reduce Credit Lines?

There are several reasons why credit card issuers may decide to lower your credit limit after a period of inactivity. Let’s take a closer look at some of the primary factors:

1. Risk Management

Credit card companies are in the business of managing risk. When a credit card goes unused for an extended period, issuers may consider it a potential risk. They may assume that a customer who is not using their card is less likely to make timely payments or may be at risk of financial difficulty. In this case, reducing the credit line is a precautionary measure to protect the issuer from potential losses.

2. Inactive Accounts Are Expensive to Maintain

Credit card issuers have operational costs associated with managing accounts. This includes maintaining records, processing statements, and offering customer service. If you are not using your credit card and there’s little or no activity on the account, the issuer may decide to reduce your credit limit as a way to cut costs. By reducing credit lines on inactive accounts, the issuer can minimize the expenses associated with accounts that don’t generate revenue.

3. Credit Card Issuers Want to Encourage Usage

Credit card issuers earn money from your card transactions, especially through interest, fees, and interchange fees from merchants. If you haven’t been using your credit card for a while, the issuer may reduce your credit limit to encourage you to use the card more actively. This reduction can be a strategy to prompt you to reconsider using the card and start making purchases again.

4. Changes in Your Credit Profile

Another reason for a credit line reduction could be changes in your credit profile. If your credit score drops or your financial situation changes (such as a reduction in income), credit card issuers may reduce your credit limit to align with the new level of risk. The issuer might have access to your updated financial information, which could trigger a reevaluation of your creditworthiness.

5. Credit Card Issuer’s Internal Policies

Each credit card issuer has its own policies when it comes to managing credit limits. Some issuers may have a policy of automatically reviewing and reducing the credit lines of accounts that haven’t had any activity for a certain period, such as six months or a year. These policies are typically in place to ensure that the bank is only extending credit to active and financially healthy customers.

6. Economic Factors

Economic conditions can also play a role in credit line reductions. During periods of economic uncertainty or financial instability, issuers may adopt more conservative lending practices. In these cases, even customers who have historically been in good standing might see their credit limits reduced. This is a response to broader economic trends and is not necessarily a reflection of your personal financial habits.

How a Reduced Credit Line Affects Your Credit Score

A reduction in your credit limit can have several consequences on your credit score. Let’s look at some of the main ways it can impact your creditworthiness:

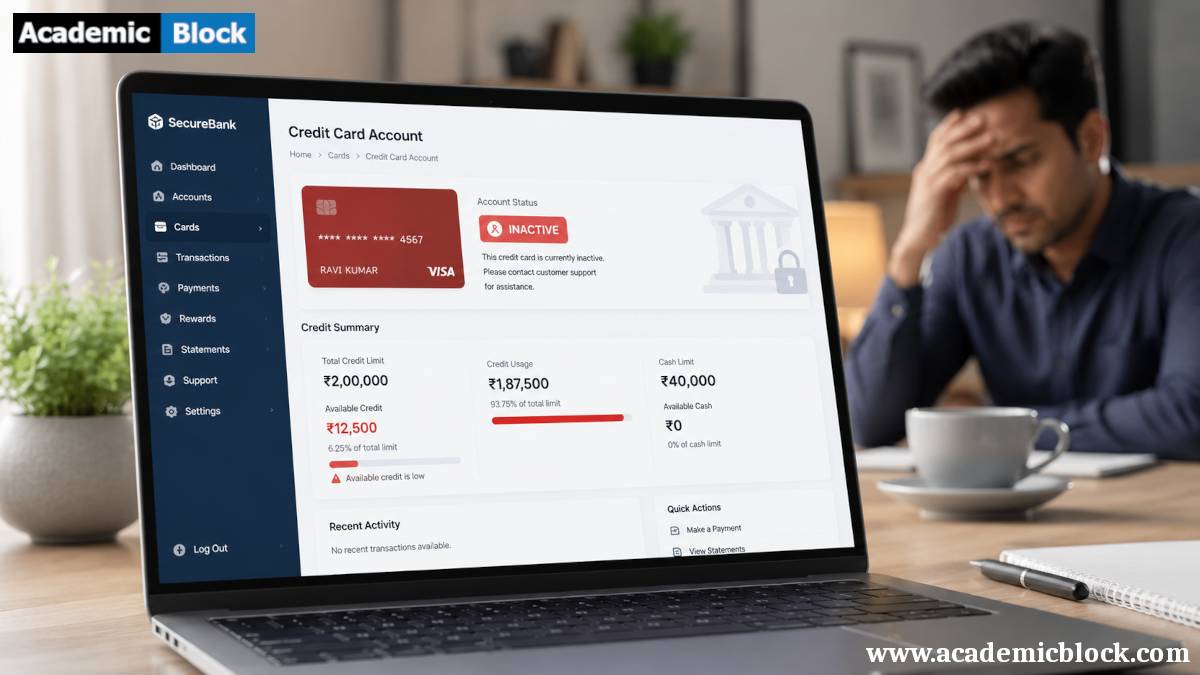

1. Credit Utilization Ratio

One of the most significant factors that influence your credit score is your credit utilization ratio. This ratio is the percentage of your total credit limit that you are using at any given time. For example, if your credit card has a limit of $5,000 and you carry a balance of $1,000, your credit utilization ratio is 20%. Credit scoring models like FICO generally recommend keeping your credit utilization below 30% to maintain a healthy score.

When your credit limit is reduced, your credit utilization ratio may increase, even if your spending habits remain the same. For instance, if your limit is cut from $5,000 to $3,000, but your balance remains $1,000, your utilization ratio will jump to 33%. This can negatively impact your credit score, as it suggests you are using a higher portion of your available credit.

2. Impact on Your Credit History Length

Another factor that affects your credit score is the length of your credit history. Creditors value long-standing accounts because they demonstrate your ability to manage credit over time. A credit line reduction might be a sign that the issuer is no longer interested in keeping the account active, which could lead to a closure of the account if it remains inactive for too long. Closing an old account can shorten your credit history and potentially reduce your credit score.

3. Hard Inquiry Risk

In some cases, when a credit card issuer reduces your credit limit, it may trigger a hard inquiry on your credit report. This can occur if the issuer needs to check your creditworthiness before making any changes. Although a hard inquiry generally has a minor and temporary effect on your credit score, it could still cause a slight dip in your score.

How to Prevent Credit Line Reductions

While you can’t control every factor that affects your credit line, there are steps you can take to reduce the likelihood of having your credit limit reduced due to inactivity:

1. Use Your Card Regularly

The simplest way to avoid a reduction in your credit limit is to use your credit card regularly. You don’t need to make large purchases—just small, consistent purchases like gas, groceries, or a subscription service. By using your card, even for minor purchases, you signal to the issuer that the account is active and valuable.

2. Make at Least the Minimum Payment

If you’re not using your card often, ensure that you still make at least the minimum payment each month. This demonstrates to the issuer that you are managing your account responsibly, even if you’re not spending much.

3. Keep Your Credit Card in Good Standing

Always aim to maintain a healthy credit score by paying your bills on time, keeping your credit utilization low, and avoiding late fees. This will make you less of a risk in the eyes of your credit card issuer and increase the chances of retaining your credit line.

4. Request a Higher Limit

If your credit line has been reduced, and you want to restore it, consider contacting your credit card issuer to request a credit limit increase. If your financial situation has improved or your credit score has gone up, the issuer may be willing to raise your limit again.

5. Monitor Your Credit Activity

Stay on top of your credit card activity by checking your statements and credit reports regularly. If you notice any changes, such as a reduced credit line, reach out to your issuer to discuss the issue and understand the reason behind the reduction.

Final Words

Credit card issuers may reduce credit lines after periods of inactivity for a variety of reasons, including risk management, cost-cutting, and encouraging usage. While this can affect your credit score due to changes in your credit utilization ratio, understanding the reasons behind credit line reductions can help you take steps to prevent them. By staying active with your credit card, making timely payments, and keeping an eye on your credit activity, you can maintain a healthy credit profile and avoid unwanted changes to your credit limit. Please provide your comments below, it will help us in improving this article. Thanks for reading!

Questions and Answers related to Credit Card Credit Lines Are Reduced After Inactivity:

A credit line is the maximum amount a credit card issuer allows you to borrow. It determines your purchasing power and financial flexibility, influencing credit utilization and your credit score. Responsible use of the credit line, such as timely repayments, helps improve financial health and creditworthiness.

A $500 credit line means you can borrow up to $500 on your credit card. It is ideal for limited spending and controlled financial management. Staying within this limit and repaying promptly ensures better credit health and potentially higher credit limits in the future.

A $5000 credit line allows you to make purchases or withdraw funds up to $5000. It provides greater financial flexibility for larger expenses. Proper management of this credit line by staying under the limit and repaying on time can positively impact your credit score.

A $1000 credit line signifies the maximum amount you can spend or borrow using your credit card, capped at $1000. It’s a manageable limit for small expenses. Timely repayment builds your credit profile and may lead to higher credit lines in the future.

A Discover credit line refers to the maximum credit limit available on a Discover card. It varies based on creditworthiness, income, and usage. Managing your Discover card responsibly ensures better benefits, higher credit lines, and an enhanced credit score.

Most issuers do not allow you to exceed your credit limit unless you opt-in for over-limit protection. Even then, fees may apply. Staying within your limit prevents penalties, protects your credit score, and ensures financial discipline.

Credit limit and credit line are related but distinct. Credit line is the overall borrowing capacity, while credit limit is the maximum spendable amount. Both are essential for financial management, but the choice depends on your borrowing needs and repayment habits.

To apply for a Chase line of credit, visit their website or branch. Ensure you meet eligibility criteria like income proof and credit score. Submit the required documentation and await approval. A strong credit profile increases your chances.

High credit line credit cards include the Chase Sapphire Reserve, Capital One Venture, and American Express Platinum. These cards offer significant credit limits and rewards, ideal for those with excellent credit scores and high spending needs.

Capital One’s line of credit interest rates vary depending on your creditworthiness and the type of product. Rates typically range from 9.99% to 24.99%. Always review terms and conditions before applying for a Capital One credit product.

To apply for a PayPal line of credit, visit PayPal Credit’s website. Log in to your PayPal account, navigate to “PayPal Credit,” and complete the application. Ensure you meet the eligibility criteria, including a good credit score and income proof. Approval depends on creditworthiness.

To increase your Capital One credit line, log into your account, navigate to the “Request Credit Line Increase” section, and submit your request. Factors like payment history, credit utilization, and income will be evaluated. Responsible usage increases approval chances.

To request a Chase credit line increase, log into your account or call customer service. Provide updated income details and explain why you need the increase. A strong credit history and low utilization rate improve your chances of approval.

The American Express credit line varies depending on factors like your credit score, income, and payment history. Typically, their credit lines range from $1,000 to $50,000 or more for premium cardholders. Managing your credit responsibly can help increase the limit.

Your credit limit may increase automatically due to consistent on-time payments, low credit utilization, or positive updates to your credit score and income. Lenders reward responsible credit usage with higher limits to build loyalty and encourage spending.

To apply for a Chase Bank credit line online, visit Chase’s website, log in, and navigate to “Apply for a Credit Line.” Complete the application with details like income, employment, and financial history. Ensure a good credit score to boost approval odds.

Getting an American Express line of credit is relatively straightforward for applicants with a high credit score (700+), stable income, and positive financial history. Ensure you meet the eligibility criteria and provide accurate documentation to increase approval chances.

Obtaining an American Express business line of credit requires excellent credit (750+), a profitable business, and proof of stable cash flow. While challenging, strong financial documentation and a positive credit history increase approval likelihood significantly.

To apply for a Wells Fargo credit line, visit their website or branch. Provide financial details like income, business revenue (if applicable), and credit history. Approval depends on creditworthiness, with higher scores and stable income increasing your chances.

The limit on an American Express business line of credit typically ranges from $10,000 to $250,000, depending on factors like business revenue, credit score, and repayment history. Higher financial stability often secures greater credit limits.

To apply for an instant credit line online with no credit check, consider alternative lenders like secured credit cards or fintech platforms. Submit proof of income and identity. Note that terms may include higher fees or collateral requirements.