How to Use Debit Cards for Paying Off Installment Loans

Overview

Paying off an installment loan with a debit card is a straightforward and convenient method for many borrowers. Traditionally, installment loans are repaid using checks, direct bank transfers, or other conventional methods. However, as technology advances, financial institutions are increasingly allowing the use of debit cards for such payments. This article by Academic Block will explore the steps involved, the benefits, potential challenges, and considerations when using a debit card to pay off installment loans.

Understanding Installment Loans

Before delving into how debit cards can be used for repayment, it’s important to understand what installment loans are. Installment loans are types of credit where the borrower agrees to repay the loan amount in regular, fixed installments over a set period. Common examples include car loans, student loans, mortgages, and personal loans. These loans typically have a specified interest rate and term, with monthly or biweekly payments. While traditional repayment methods like bank transfers or checks are common, paying off an installment loan with a debit card can be an attractive option for those who prefer digital payments.

Can You Use a Debit Card to Pay Off an Installment Loan?

In many cases, yes, you can use your debit card to make payments on installment loans. However, whether this option is available depends on your loan provider and the payment system they use. Some lenders accept debit card payments directly, while others may require you to use a third-party service. Let’s break down the steps involved.

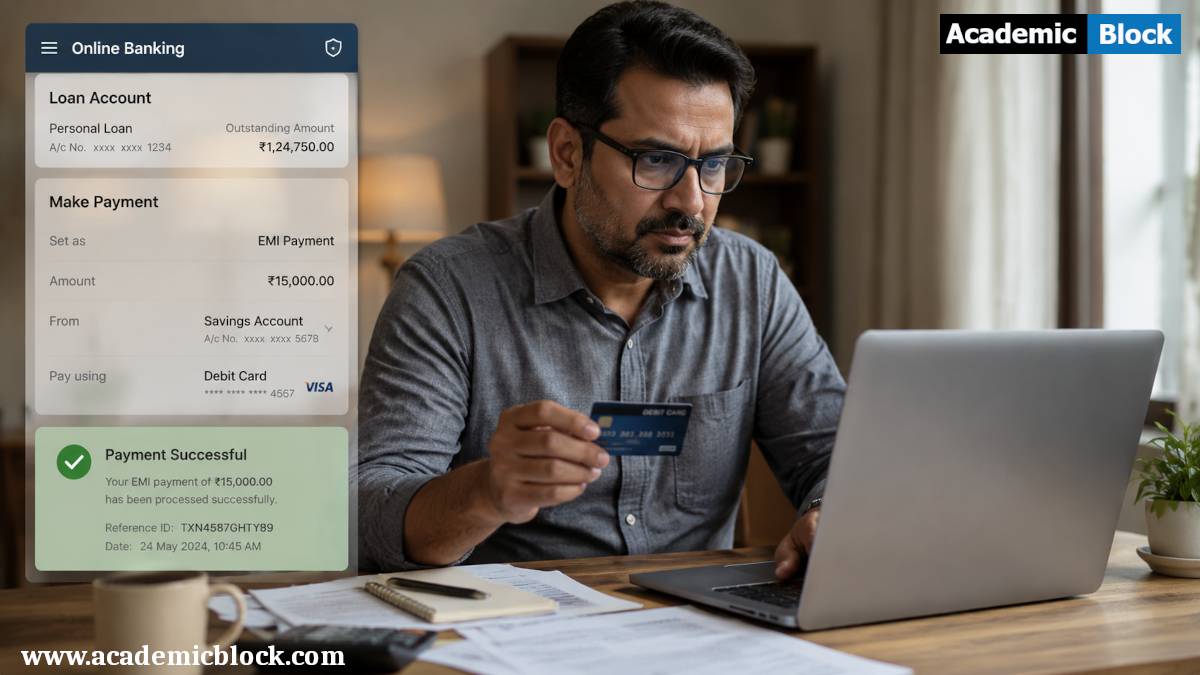

Steps to Pay an Installment Loan with a Debit Card

-

Check Your Loan Provider’s Payment Options : The first step is to verify with your lender if debit card payments are allowed. Many financial institutions and loan servicers have online portals where you can check your payment options. If they don’t directly accept debit card payments, they may allow you to use a third-party payment processor like Western Union or PayPal, which can facilitate payments via your debit card.

-

Gather Your Debit Card Information : To make the payment, ensure you have your debit card on hand. Debit cards are linked to your checking account, and the payment will be deducted directly from your available balance. Make sure you have sufficient funds in your account to avoid overdraft fees or failed payments.

-

Navigate to the Payment Portal : If your lender accepts debit card payments directly, navigate to their online payment portal. This may require you to log into your account using your username and password. Look for the “Pay Now” option or something similar that allows you to make a payment.

-

Enter Your Debit Card Details : Once you’ve accessed the payment page, select the option to pay with a debit card. You will need to enter your card number, expiration date, CVV (the three-digit security code), and the billing address associated with the card. Double-check all the information for accuracy before proceeding.

-

Select the Payment Amount : Some lenders may allow you to make a partial payment, while others may require full payment for the installment. If you are only paying part of the installment, make sure you specify the correct amount. Check your loan terms to ensure that making a partial payment won’t affect your loan schedule or incur additional fees.

-

Confirm the Payment : Before completing the transaction, confirm all details, including the payment amount and your card information. Once everything looks correct, click the “Submit” or “Pay Now” button. The system will process the payment, and you should receive a confirmation email or receipt.

-

Check Your Bank and Loan Account : After making the payment, check both your bank account and loan account to ensure the transaction was successfully completed. The amount should be deducted from your checking account balance, and your loan account should reflect the payment.

Benefits of Using Debit Cards for Loan Payments

-

Convenience : Paying with a debit card is often faster and more convenient than traditional methods like checks or money orders. You can complete the transaction from anywhere with an internet connection, whether you’re at home, at work, or on the go.

-

Instant Payment Processing : Unlike checks or other methods that might take a few days to clear, debit card payments are processed almost instantly. This means that your payment is recorded by the lender quickly, ensuring that you stay current on your loan and avoid late fees.

-

Automatic Payment Tracking : When you use a debit card, your payment will be tracked automatically by both your bank and the lender. This helps you avoid losing receipts and provides you with an electronic record for your financial records or tax purposes.

-

Avoiding Late Fees : Debit card payments often ensure that your payments are processed on time, as there’s no waiting for a check to clear or for a money order to be sent and received. This reduces the risk of incurring late payment fees.

Potential Challenges of Using Debit Cards for Loan Payments

While paying off an installment loan with a debit card offers many advantages, there are some challenges and limitations to consider:

-

Transaction Fees : Some loan providers or third-party payment processors charge a fee for processing debit card payments. These fees can add up, particularly if you make multiple payments. It’s essential to check if there are any hidden fees before choosing this payment method.

-

Overdraft Risks : Since payments are deducted directly from your checking account, there is a risk of overdrafting if you don’t have enough funds in your account. Overdraft fees can be expensive and may complicate your financial situation. Always ensure that you have enough balance before making a payment.

-

Payment Processing Delays : Although debit card payments are generally processed quickly, some lenders may have specific processing times or limitations that can cause delays. It’s important to review your lender’s payment policy to understand how long it takes for payments to be reflected on your loan balance.

-

Debit Card Limitations : Some debit cards may have limits on the amount you can spend per transaction or per day. If your loan installment amount exceeds the transaction limit, you might need to split the payment across multiple transactions, which could lead to extra fees.

Alternatives to Debit Card Payments

If using a debit card is not an option or if you want to explore other methods, here are some alternatives:

-

Bank Transfers : Most loan providers accept bank transfers, where you can transfer funds directly from your checking or savings account to your loan account. This method is typically free of transaction fees and is a secure way to ensure your payment is made.

-

Checks : Paying by check is still a common option, though it may take a few days to clear. Ensure you keep a record of your payment and verify with the lender that it has been received and processed.

-

Automatic Payment Setups : Setting up automatic payments from your checking account can help ensure you never miss an installment. Many lenders allow you to set up a recurring payment schedule that will automatically withdraw funds from your account on the due date.

Final Words

Paying off installment loans with a debit card is convenient, offering instant processing and easy tracking. However, it may involve fees, overdraft risks, and card limitations. Check your lender’s policies, ensure sufficient funds, and consider alternatives like bank transfers or automatic payments to manage your loan effectively. We value your feedback! Please leave a comment to help us enhance our content. Thank you for reading!

Questions and Answers related to Use Debit Cards for Paying Off Installment Loans:

To pay installment loans with a debit card, log into your lender’s portal, navigate to the payment section, and select the debit card option. Enter the required card details, including card number, expiration date, and CVV. Verify the amount and confirm the transaction to complete payment.

Some lenders may charge convenience fees for using a debit card to pay installment loans, typically a percentage of the transaction amount. Check your lender’s payment terms to confirm if fees apply. Many lenders offer fee-free options such as direct bank transfers or checks.

Most personal loans, auto loans, and payday loans accept debit card payments. However, some mortgage and student loan providers may restrict debit card usage. Check with your lender to confirm accepted payment methods for your specific type of installment loan.

Yes, some lenders allow loans to be paid off using a credit card balance transfer. This method can consolidate debt and reduce interest if the credit card offers promotional rates. Confirm with your lender and credit card issuer to ensure compatibility and avoid additional fees.

Using a debit card for installment payments is generally safe and convenient. It ensures immediate withdrawal from your account, reducing the risk of missed payments. However, confirm with your lender that they accept debit cards and check for any associated convenience fees.

Yes, you can pay off a loan using a debit card if your lender allows this payment method. Ensure sufficient funds are available in your account and confirm if there are any fees for using a debit card. Check with the lender for early payment policies.

To set up automatic installment payments with a debit card, log into your lender’s online portal or contact customer service. Provide your debit card details and authorize recurring payments. Confirm the schedule and ensure your account has sufficient funds to avoid declined transactions.

Yes, you can pay off your installment loan early using a debit card if your lender permits early payments. Check the loan agreement for prepayment penalties or fees. Early payoff can save interest costs, making it a beneficial option for borrowers with excess funds.

Before using a debit card for loan payments, confirm with your lender that they accept debit cards and check for associated fees. Verify your account balance to ensure sufficient funds and review the payment schedule to avoid late payments or declined transactions.

Some lenders impose limits on debit card payments, such as maximum transaction amounts or daily limits. These restrictions ensure security and prevent overdrawn accounts. Check with your lender and bank to understand any limits that may apply to debit card transactions.

To avoid declined transactions, ensure sufficient funds are available in your account before payment. Verify card details and check for expiration. Monitor daily spending limits and contact your bank to resolve any potential blocks or issues affecting your debit card.