What to Do if Your Card Is Lost or Stolen: Debit or Credit

Overview

Losing a debit or credit card can be a stressful and alarming experience, but it’s essential to act quickly to minimize the potential damage. Whether your card was lost or stolen, taking immediate action can help protect your finances and personal information from fraud. This article by Academic Block will outlines the key steps you should take if you find yourself in such a situation.

1. Stay Calm and Assess the Situation

The first thing to remember when you realize your card is missing is to stay calm. Panicking won’t help, but acting swiftly is crucial. If you’ve misplaced your card, retracing your steps to see if you can find it may be worthwhile, but don’t waste too much time on this. If your card was stolen, time is of the essence in preventing unauthorized transactions.

2. Report the Loss or Theft to Your Bank or Card Issuer

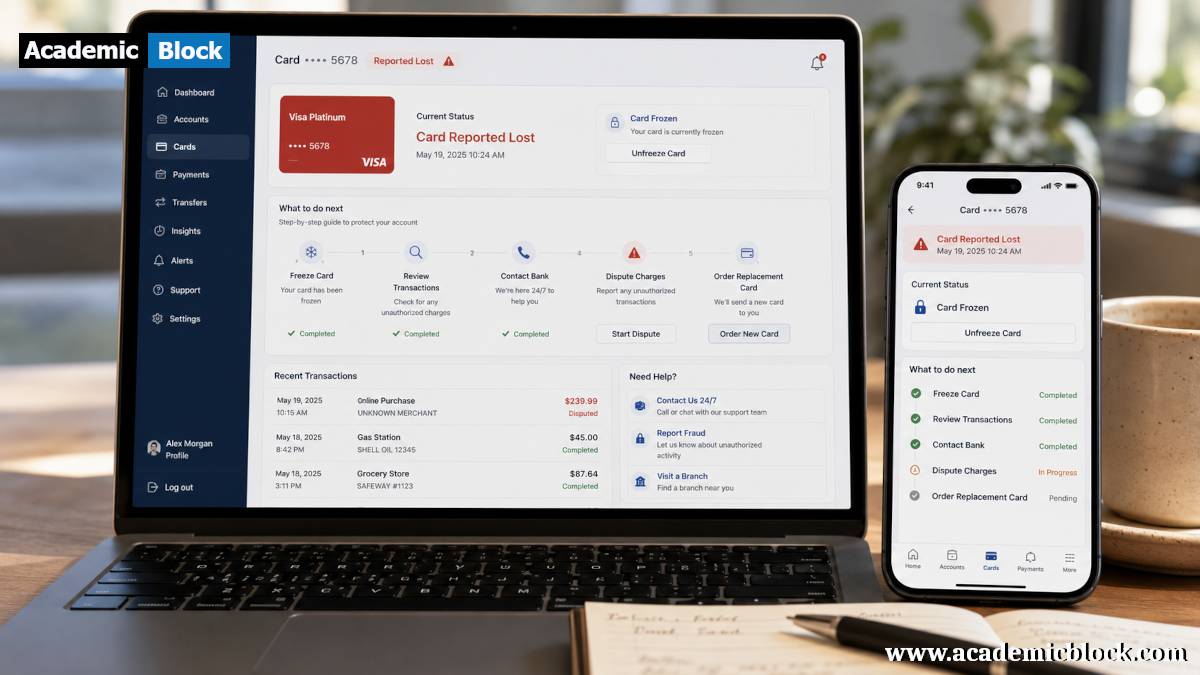

Once you’ve determined your card is missing, the next step is to contact your bank or card issuer immediately. Both debit and credit card companies have 24/7 customer service hotlines that you can call to report a lost or stolen card. You can often find these numbers on the back of your card, on your statement, or online. Most financial institutions provide an option to lock or block your card instantly.

Why It’s Important:

-

Immediate Blocking: Reporting your card as lost or stolen will prevent any further transactions from being processed, which could save you from significant financial loss.

-

Fraud Protection: Many banks have fraud protection policies that limit your liability for unauthorized charges, but only if you report the issue promptly.

3. Freeze or Lock Your Card

Many banks and credit card issuers allow you to freeze or lock your card temporarily through their mobile apps or online banking services. This can be especially helpful if you’ve misplaced your card and believe it might still turn up. A lock prevents anyone from using it for purchases until you unlock it.

For a more secure approach, you can request a full cancellation of the card and ask for a new one, especially if you suspect the card has been stolen.

4. Request a Replacement Card

After reporting the loss, your bank or card issuer will typically issue you a replacement card. This process can take anywhere from a few days to a couple of weeks, depending on your bank’s procedures. If you rely on your card for everyday purchases or bills, it might be worth asking if they can expedite the replacement process.

In some cases, you may be able to use a temporary card or access a digital card number to continue making transactions while waiting for the physical replacement.

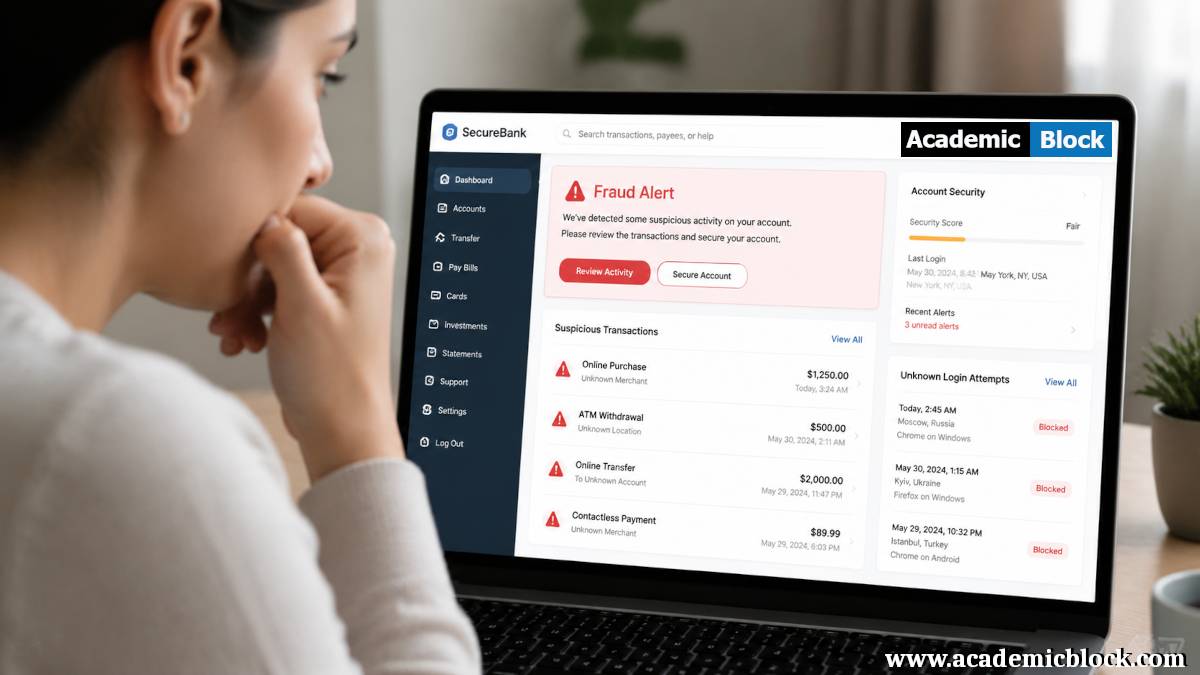

5. Monitor Your Account for Fraudulent Transactions

Even after reporting a lost or stolen card, it’s crucial to monitor your bank account or credit card statements for unauthorized charges. Review all recent transactions carefully and report any suspicious activity immediately. Most banks will refund fraudulent charges, but they typically require documentation and proof that you reported the loss promptly.

Key Actions:

-

Use Online Banking: Frequently check your account via online banking to spot any new charges.

-

Set Up Alerts: Set up transaction alerts via email or SMS to notify you of any charges made to your account.

6. Dispute Unauthorized Charges

If your card was used fraudulently before you reported it missing, you must dispute the charges. Most banks and credit card companies have procedures for handling disputes. You will likely be required to fill out a form, provide details of the unauthorized transactions, and may need to submit a formal statement.

It’s important to act quickly to dispute any unauthorized charges, as there are time limits for filing claims. In general, you may have up to 60 days after the statement date to report fraudulent charges on your credit card. For debit cards, the time window is often shorter, with many banks requiring reports to be made within two business days.

7. File a Police Report (If Applicable)

If your card was stolen or if you are the victim of identity theft, it might be a good idea to file a police report. A police report can help provide additional protection in case of ongoing fraud and serve as documentation for your bank or credit card issuer. While not all situations require a police report, it can be helpful in more serious cases.

8. Prevent Future Loss or Theft

Once your card is reported, replaced, and any fraudulent charges have been disputed, it’s essential to take steps to prevent future incidents. Here are a few preventive measures:

-

Use Mobile Payment Solutions: Services like Apple Pay, Google Pay, or Samsung Pay can offer an added layer of security, as they often require biometric authentication (fingerprint or facial recognition) for transactions.

-

Avoid Carrying Unnecessary Cards: Only carry the cards you use regularly, and store others in a secure place.

-

Activate Two-Factor Authentication: Many banks and card issuers offer two-factor authentication (2FA) for online transactions. This adds an extra layer of security by requiring you to confirm transactions through an additional method, such as a text message or email.

9. Protect Your Identity

In cases of theft, your personal information might be at risk. If you believe your identity has been compromised, take immediate steps to protect yourself:

-

Place a Fraud Alert: Contact one of the three major credit bureaus (Experian, Equifax, or TransUnion) to place a fraud alert on your credit report. This will alert lenders and creditors to verify your identity before granting credit in your name.

-

Monitor Your Credit: Request a free credit report to review any new accounts or inquiries made in your name. This will help you spot any potential identity theft early.

-

Consider a Credit Freeze: A credit freeze prevents creditors from accessing your credit report, which can make it harder for fraudsters to open new accounts in your name.

10. Know Your Rights and Liabilities

When it comes to lost or stolen cards, both debit and credit cardholders are afforded certain protections under the law. The extent of your liability depends on the type of card and how quickly you report the loss.

-

Credit Cards: Under the Fair Credit Billing Act (FCBA), your liability for unauthorized charges is limited to $50, and if you report the theft within 60 days, you may be held harmless for any fraudulent charges.

-

Debit Cards: The Electronic Fund Transfer Act (EFTA) offers protection for debit cardholders, but the timeline for reporting is stricter. If you report within two business days, your liability is limited to $50. After two days, your liability could rise to $500 or more.

Final Words

Losing a debit or credit card can be unnerving, but by acting quickly and following the steps outlined above, you can minimize the potential damage. Reporting the loss or theft promptly, monitoring your accounts, and disputing fraudulent charges are crucial to protecting yourself financially. We value your feedback! Please leave a comment to help us enhance our content. Thank you for reading!

Questions and Answers related to What to Do if Your Card Is Lost or Stolen:

If you lose your debit card, contact your bank immediately. They will block your card and help you order a replacement. Keep track of any unauthorized transactions to report them promptly. Additionally, you can place a fraud alert or freeze your account to prevent further issues. Most banks also offer alerts for any suspicious activity on your account.

If you lose your credit card, report it immediately to your issuer. Most financial institutions offer 24-hour customer service to assist you. After reporting, they will cancel the lost card and issue a new one. It’s crucial to check your statements for fraudulent charges and dispute any unauthorized transactions. Freezing your card may also be an option to protect your funds while waiting for a replacement.

To report a stolen credit card, contact your credit card issuer’s customer service or fraud department immediately. Most companies have 24/7 support. When reporting, provide details about the theft and any suspicious transactions. The issuer will block your card, issue a replacement, and may help you dispute unauthorized charges. Be sure to monitor your account and credit reports for unusual activity.

If your credit card is lost, act quickly to minimize financial loss. First, report the loss to your credit card issuer. They will freeze your account and issue a replacement card. Monitor your account for any unauthorized transactions, and notify the issuer of any fraudulent charges. It’s also wise to place a fraud alert or freeze on your credit to further protect yourself.

Yes, many banks offer the option to freeze your debit card if it’s stolen. This is a helpful security measure that prevents unauthorized transactions while you await a replacement. If freezing your card isn’t available, contact your bank immediately to block the card and initiate the process for issuing a new one. Be sure to also review recent transactions for any fraud.

After losing your debit card, protect your finances by reporting it to your bank immediately. The bank will freeze your account and issue a new card. Review your account for unauthorized transactions and dispute any fraudulent charges. Consider placing a fraud alert on your credit report. Additionally, change any relevant passwords and PINs to further protect your financial security.

To cancel a lost or stolen credit card, contact your card issuer’s customer service as soon as possible. Most issuers have dedicated fraud departments available 24/7. They will immediately block the card and prevent further unauthorized transactions. Request a new card and monitor your account closely for any suspicious activity. Some issuers may require you to fill out a fraud report.

To get a replacement debit card, contact your bank immediately. They will block your current card and order a new one for you. You may need to provide identification and details of the loss. Some banks offer expedited shipping for a replacement card. In the meantime, monitor your account for any unauthorized transactions and dispute them promptly.

While it is not always necessary to report a stolen card to the police, it can be useful in cases of significant fraud or identity theft. Some credit card issuers may request a police report for investigation purposes, especially if large sums are involved. Always check with your bank or credit card company for their specific requirements on reporting theft.

Yes, you can get lost debit card charges refunded if you report the theft to your bank promptly. The bank will investigate the unauthorized charges and, in many cases, refund the amount. However, this process may take time. Be sure to notify your bank as soon as you realize your card is lost, and provide details of any fraudulent transactions for faster resolution.

If your credit card is lost or stolen, report it to the issuer immediately. Most issuers will freeze your account and issue a new card. Your rewards should remain intact, but check with the issuer to confirm. You may also need to update payment information for any recurring charges.

If your card is lost, contact your card issuer immediately to temporarily disable contactless payments. Many banks offer options through their mobile app or website to block the card. Alternatively, you can request a freeze on the card’s transactions. This prevents unauthorized contactless payments while you resolve the issue.