When Debit Card Purchases Are Charged in Installments

Overview

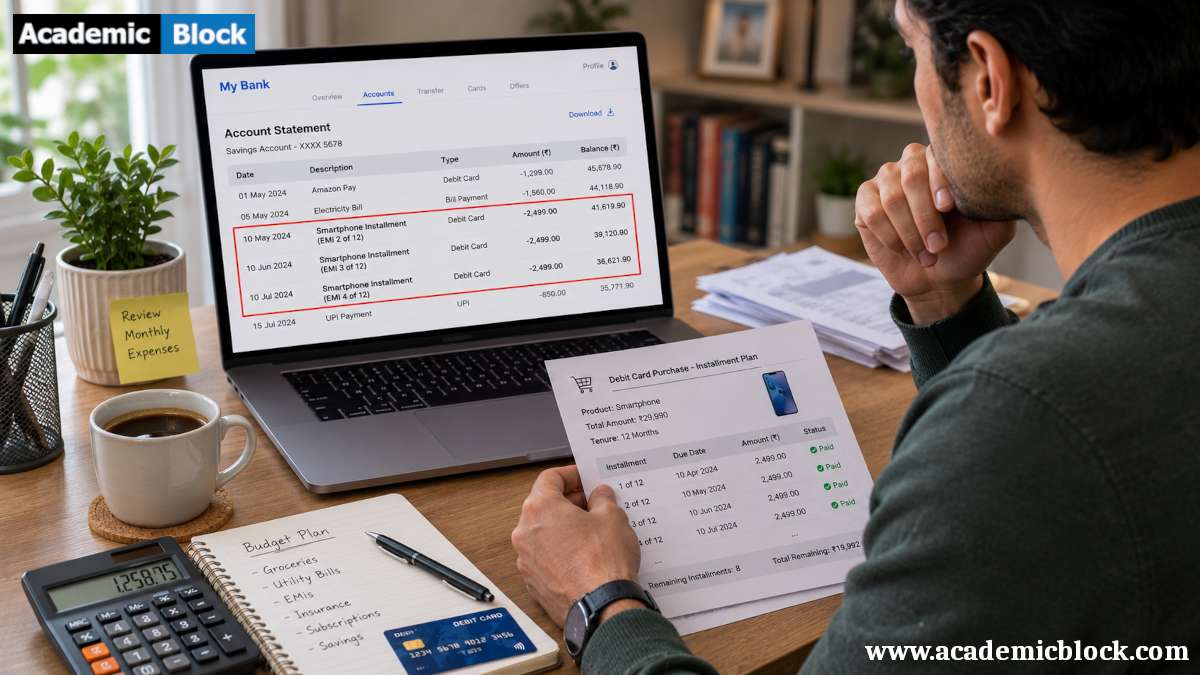

When you make a purchase using your debit card, it’s typically a one-time transaction where the full amount is deducted from your bank account immediately. However, what happens if you want to buy something expensive and prefer to pay it off in installments? Thanks to evolving payment solutions, many consumers now have the option to split their debit card purchases into smaller payments, making it easier to manage larger expenses.

In this article by Academic Block, we’ll explore what debit card purchases in installments mean, how they work, their benefits, and potential considerations before opting for this payment method.

What is a Debit Card Purchase in Installments?

A debit card purchase in installments is a financing option that allows you to break down the cost of a large purchase into manageable, periodic payments. Instead of paying the full amount at once, you can spread the payments over weeks or months, depending on the terms offered. This option has become increasingly popular, especially for high-ticket items like electronics, appliances, or even travel bookings.

How Do Debit Card Purchases in Installments Work?

-

Making the Purchase : When you select the items you want to buy, you will be given an option to pay in installments at the checkout. This could either be at a physical store or online.

-

Approval and Authorization : Once you choose the installment option, you will typically need to authorize the full purchase on your debit card. The bank or the payment provider will only deduct the first installment from your account upfront. Future payments are scheduled automatically based on the terms of the agreement.

-

Automatic Deductions : Payments are usually automatically deducted from your bank account on the agreed-upon due dates. You won’t have to worry about missing payments unless your account doesn’t have enough funds.

-

Interest-Free (In Most Cases) : Many debit card installment plans do not carry interest, unlike credit card installment plans. However, some programs might involve small fees, so it’s important to read the fine print.

Benefits of Debit Card Purchases in Installments

-

No Credit Card Required : Debit card installment plans are perfect for consumers who do not have credit cards or prefer not to use them. It allows people without access to traditional credit cards to manage large purchases more easily.

-

Interest-Free Financing : Unlike credit card payments, which may come with high-interest rates, debit card installment plans are often interest-free, which makes them a more affordable way to spread out payments. However, some plans may charge a small processing fee, so it’s always important to check the terms.

-

Manageable Payments : Breaking down a big purchase into smaller, scheduled payments can make it easier to manage your monthly budget. This allows you to buy what you need without impacting your bank balance too heavily at once.

-

Instant Approval : Many debit card installment plans don’t require a credit check. As long as your debit card is linked to a sufficient bank account balance, you can often get instant approval for a payment plan, making it a faster and more accessible option than credit cards.

-

No Risk of Debt : Since you are paying directly from your bank account, you are only spending money you already have. This reduces the risk of accumulating debt that you might face with credit cards.

Potential Downsides of Debit Card Purchases in Installments

-

Insufficient Funds : If your bank account doesn’t have enough funds when an installment is due, you might face overdraft fees or other penalties. This is something to be cautious about, as failing to make payments could also lead to the plan being canceled or your purchase being marked as unpaid.

-

Limited Retailer Availability : Debit card installment options aren’t available everywhere. You will likely need to shop at specific retailers or use payment processors that partner with banks offering these services.

-

Hidden Fees : While most debit installment plans are interest-free, some may have hidden processing or late-payment fees. Be sure to check all terms carefully before committing to a plan.

-

No Credit Score Benefits : One limitation of using a debit card for installment payments is that, unlike credit card payments, these purchases do not get reported to credit bureaus. This means you won’t be able to build or improve your credit score through debit card installment plans.

Where Can You Use Debit Card Purchases in Installments?

Debit card installment plans are typically available for high-ticket items like:

-

Electronics : Smartphones, laptops, and TVs.

-

Home Appliances : Refrigerators, washing machines, and ovens.

-

Furniture : Sofas, dining tables, and beds.

-

Travel : Flights, hotel bookings, and vacation packages.

-

Education : Online courses, books, and study materials.

Steps to Use Debit Card Purchases in Installments

-

Check If the Retailer Offers Installments : Before making a purchase, confirm that the retailer offers an installment payment plan for debit card purchases. This is often available at checkout or can be found in the retailer’s payment options.

-

Select the Installment Option : Choose the number of installments (such as 3, 6, or 12 months) that best suits your budget.

-

Review Terms and Conditions : Always review the terms carefully. Check for any fees, the installment schedule, and penalties for late payments.

-

Make Your Purchase : Once you’ve agreed to the terms, authorize the transaction using your debit card.

-

Monitor Your Payments : Ensure there are sufficient funds in your account for future payments. If not, you may incur penalties or miss a payment.

Tips for Using Debit Card Installments Responsibly

-

Budget Your Payments : Before committing to any installment plan, calculate whether you can comfortably manage the monthly payments based on your income and expenses.

-

Read the Fine Print : Always read the full terms and conditions of the installment plan. Ensure you’re clear about any processing fees, late payment penalties, or restrictions on the installment plan.

-

Track Your Payments : Setting reminders for payment dates can help you avoid penalties or late fees. Many banks also allow you to view and manage your payment schedule through their mobile apps.

-

Use Installments for Essential Purchases : Installment plans should be used for necessary items or planned purchases, not impulse buys. Overusing installment plans can strain your budget and finances.

How Debit Card Purchases in Installments Compare to Credit Card Purchases

Approval Process

-

Debit Card Purchases : Typically, no credit check is required, as long as your debit card is linked to a sufficient bank balance.

-

Credit Card Purchases : Requires a credit check, and approval depends on your credit score and creditworthiness.

Interest Charges

-

Debit Card Purchases : Often interest-free, though some plans may have small processing fees or charges if the payment plan is extended.

-

Credit Card Purchases : Usually comes with interest charges if the balance is not paid in full by the due date, making it more expensive over time.

Risk of Debt

-

Debit Card Purchases : Low risk of accumulating debt, as payments are deducted directly from your bank account. You can only spend what you have.

-

Credit Card Purchases : Higher risk of debt, as it’s easy to overspend, and interest charges can lead to significant debt accumulation if not managed properly.

Credit Score Impact

-

Debit Card Purchases : No impact on your credit score, as debit card payments are not reported to credit bureaus.

-

Credit Card Purchases : Timely payments can improve your credit score, while missed or late payments can damage it.

Eligibility

-

Debit Card Purchases : Requires a sufficient balance in your linked bank account to cover each installment.

-

Credit Card Purchases : Requires a good credit score and available credit on your card to make purchases on installments.

Flexibility in Payments

-

Debit Card Purchases : Payments are automatically deducted from your bank account, which may offer less flexibility in terms of changing payment dates.

-

Credit Card Purchases : Some credit card companies offer more flexibility, allowing you to adjust payment schedules or change the number of installments.

Fees and Penalties

-

Debit Card Purchases : Some plans may include small processing fees, but they typically have fewer hidden costs.

-

Credit Card Purchases : May involve annual fees, late payment fees, and high-interest rates if balances aren’t cleared on time.

Final Words

Debit card purchases in installments provide a flexible and manageable way to buy items you need without the burden of paying all at once. Whether you’re shopping for electronics, home appliances, or travel, this payment method can offer greater control over your finances.

Before opting for an installment plan, be sure to understand the terms, check for hidden fees, and ensure your bank account has enough funds to cover future payments. By using this option responsibly, you can make big purchases without overextending your budget. Hope you liked this article by Academic Block, please share your thought below. Thanks for Reading!

Questions and Answers related to Debit Card Purchases Are Charged in Installments:

Debit card installments can be secure if managed correctly. Many financial institutions offer secure methods, such as encryption and monitoring tools, to safeguard transactions. However, users should ensure they are using trusted platforms and stay vigilant about potential fraud risks. It is important to review the terms and conditions to understand the security measures in place and make payments through official, secure channels.

Yes, many debit card installment plans allow early repayment without penalties. By paying off the balance early, you can avoid any potential interest charges, if applicable, and reduce the overall cost of the purchase. However, it is always advisable to check the terms of the agreement, as some providers may impose early repayment fees, although these are rare for debit card plans.

Debit card purchases are typically charged in installments when the cardholder opts for a payment plan offered by the bank or retailer. This option allows the total cost of a purchase to be divided into smaller, manageable payments over time. The option is often available for larger purchases or when a special financing arrangement is made between the cardholder and the merchant or financial institution.

Yes, debit cards can be used for installments if the financial institution or merchant offers this option. The installment plan splits the cost of a purchase into smaller payments, which are deducted directly from your bank account. However, not all debit cardholders may have access to such plans, and eligibility can depend on the terms and conditions set by the card issuer or the retailer’s payment system.

If you miss a payment on a debit card installment plan, you may face penalties, late fees, or even suspension of the installment arrangement. Depending on the terms, the full amount of the remaining balance may be charged immediately, or your bank account could be charged for the missed payment. It is essential to stay on top of payment due dates to avoid these consequences.

Yes, many online retailers and financial institutions offer installment payment options for debit cardholders. These arrangements split the cost of the online purchase into smaller, regular payments. The availability of such options depends on the retailer and the payment gateway, so it’s important to confirm if this is an option before completing the transaction.

For large purchases, debit card installment plans allow you to spread the cost over a specific period, such as three, six, or twelve months. The payment is automatically deducted from your linked bank account, reducing the total financial burden. Some plans may also have interest charges, so it’s essential to read the terms and conditions of the agreement carefully to understand the cost implications.

Monthly fees associated with debit cards can be due to a variety of reasons, including the type of account or service package you have with your bank. Some banks charge monthly maintenance fees, while others might offer accounts with additional features such as premium services or installment payment options. It is important to review your bank’s terms to understand the fees associated with your debit card and consider alternatives if they are too high.

Debit card transaction fees are regulated by government agencies to ensure fair practices for consumers. These regulations govern fees for various services, including ATM withdrawals, point-of-sale transactions, and international purchases. Financial institutions must adhere to these rules and provide transparency regarding the fees they charge, ensuring that consumers are informed before making transactions.

Debit card transaction fee regulations help protect consumers by limiting the amount banks can charge for certain transactions. These regulations promote transparency, ensuring consumers understand any fees they may incur. As a result, consumers are better equipped to make informed decisions and avoid unexpected charges, ultimately fostering fairer practices in the banking and payments industry.

True. Debit card transactions are deducted directly from the cardholder’s checking account. When a purchase is made, the funds are withdrawn in real-time or within a few business days, ensuring that the cardholder only spends what is available in their account. This makes debit card purchases a more controlled form of payment compared to credit cards.

Debit card transaction fees are regulated by government authorities to ensure fairness and transparency. These regulations govern the charges associated with various transactions such as ATM withdrawals, point-of-sale payments, and international purchases. Financial institutions are required to disclose these fees, which helps consumers make informed choices and reduces the likelihood of hidden charges.

Paying for purchases in installments with a debit card offers several benefits, including making large purchases more affordable by spreading the cost over time. It allows for better budgeting, as payments are predictable and automatically deducted. Additionally, many plans do not require interest charges, making it a cost-effective alternative to credit cards. It can also help improve cash flow management for those who prefer not to carry a balance on their credit card.

Yes, you can use installment plans for online purchases if the retailer or financial institution offers this option. The availability of installment payments will depend on the terms of the transaction and the specific online platform. It is important to check whether the merchant provides such an option before completing your purchase. Many e-commerce platforms now offer flexible payment solutions for debit cardholders.

The Apple Card monthly installment plan allows users to split the purchase cost into equal monthly payments. The amount is not charged all at once. However, the terms may vary depending on the transaction, and it is important to review the payment schedule and understand the interest, if any, associated with the installment plan. It is an option for Apple products and some other eligible purchases made with the Apple Card.

Choosing between debit card installments and credit card installments depends on your financial preferences. Debit card installments offer the advantage of not accruing interest, as payments are directly linked to your checking account. Credit card installments may offer more flexibility but could come with interest charges if not paid off in time. Consider your ability to manage payments and your financial goals when making this decision.

Many debit card installment plans are interest-free, meaning you only pay the amount due in fixed installments. However, some plans may carry additional fees or penalties, especially if you miss a payment. It is essential to carefully review the terms and conditions of the plan to ensure you are aware of any hidden charges, such as setup fees, late payment penalties, or additional processing fees.