History of Credit and Debit Cards

Overview

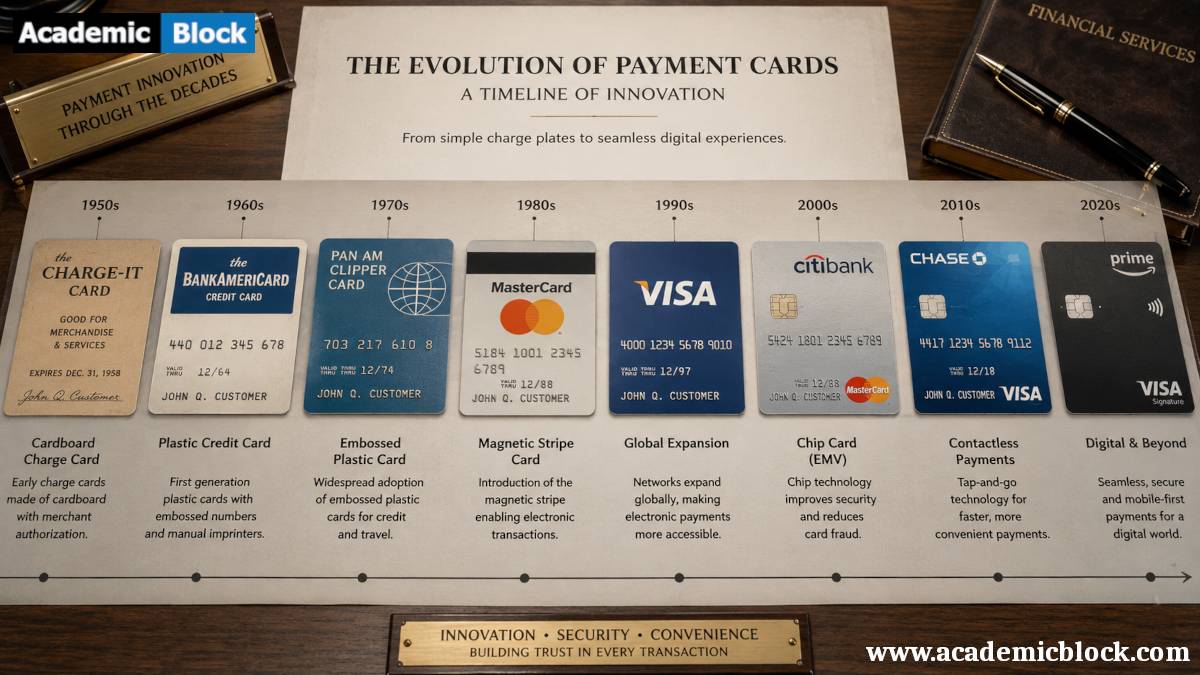

The evolution of credit and debit cards reflects the broader transformation of financial systems and consumer behavior over the last century. From their inception to their widespread adoption in today’s digital age, these plastic cards have revolutionized how consumers manage their finances, make purchases, and interact with money. This article by Academic Block will explore the history of credit and debit cards, tracing their development from early forms of credit to the sophisticated electronic payment systems we use today.

Early Forms of Credit

Credit concepts date back to ancient civilizations, where merchants allowed deferred payments. In the 1920s, U.S. businesses began issuing metal charge plates, serving as primitive credit cards. The first true credit card, the Diners Club card, was introduced in 1950 by Frank McNamara, allowing members to dine without cash. This marked a significant shift towards modern credit systems.

The Birth of Credit Cards

The first true credit card is widely regarded to be the Diners Club card, introduced in 1950. Founded by Frank McNamara, the Diners Club was initially intended for use at restaurants, allowing members to dine without cash. This innovation quickly gained popularity, leading to the expansion of the card’s acceptance at various establishments.

Diners Club was revolutionary in that it provided a simple and convenient method for individuals to access credit without requiring a prior relationship with the merchant. Following Diners Club’s success, other companies began to enter the credit card market. In 1951, the Franklin National Bank in New York issued the first bank-issued credit card, known as the Franklin Card.

The Rise of Bank Credit Cards

In the 1960s, banks began to recognize the potential of credit cards as a profitable product. Bank of America launched its BankAmericard in 1958, which would later become Visa. This initiative represented a significant shift in the credit card industry, as it established the first bank-centered model for issuing credit cards. In 1966, the card was adopted by a network of banks, paving the way for the establishment of credit card associations and networks.

Simultaneously, Mastercard (originally known as Master Charge) emerged in 1966 as a competitor to BankAmericard. These two major players would dominate the credit card market, setting standards for security, acceptance, and technology. Their influence marked the transition from individual card companies to a more interconnected system of credit cards accepted at various merchants and locations.

The Introduction of Debit Cards

While credit cards were gaining traction, the concept of debit cards emerged in the late 1960s and early 1970s. Debit cards allowed consumers to access their bank accounts directly to make purchases, providing an alternative to credit cards that required borrowing money. The first debit card was issued by the New York-based bank, the First National City Bank, in 1966, which enabled customers to withdraw cash from automated teller machines (ATMs).

The concept of using debit cards for purchases at points of sale gained momentum in the 1980s. Electronic funds transfer (EFT) technology enabled real-time transactions, allowing consumers to pay directly from their bank accounts without relying on credit. In 1983, the introduction of the Interlink network further facilitated debit card transactions, connecting various banks and merchants.

Global Expansion and Technological Advances

The 1990s saw significant growth in both credit and debit cards, aided by magnetic stripe technology. Credit card issuers began offering rewards to attract consumers, leading to increased credit card debt concerns. The introduction of EMV chip technology in the 2000s enhanced transaction security, promoting wider adoption.

The Digital Revolution

The late 1990s and early 2000s marked the rise of e-commerce, with credit and debit cards becoming the preferred payment method for online transactions. Contactless payment technology emerged, allowing users to tap cards or mobile devices for quick transactions. The COVID-19 pandemic accelerated this trend as consumers sought safer payment methods.

The Rise of Mobile Wallets

The rise of smartphones has also transformed the payment landscape. Mobile wallets, such as Apple Pay, Google Pay, and Samsung Pay, allow consumers to store their credit and debit card information digitally. By linking their cards to mobile payment apps, users can make transactions with a simple tap of their phones. This shift not only enhances convenience but also offers added security features, such as biometric authentication.

Difference Between the History of Credit and Debit Cards

The Future of Credit and Debit Cards

As technology continues to advance, the future of credit and debit cards will likely be shaped by digital wallets, biometric authentication, and cryptocurrency. Digital wallets, like Apple Pay and Google Pay, are becoming more popular as they allow users to make card payments through their smartphones or smartwatches, reducing the need for physical cards.

Additionally, biometric payment systems are on the rise, with fingerprint and facial recognition being tested as ways to authenticate cardholders without needing a PIN or signature. The integration of cryptocurrency into payment systems may also change the way we view and use traditional cards, offering a more decentralized and digital alternative to traditional banking.

Final Words

The history of credit and debit cards is a testament to the evolving nature of commerce and consumer behavior. From the early charge plates to the digital wallets of today, these payment methods have transformed how individuals manage their finances, make purchases, and interact with money. The future of credit and debit cards looks promising, with ongoing advancements in technology and security ensuring that these financial tools will continue to play a crucial role in the global economy. As consumers increasingly prioritize convenience and security, the evolution of credit and debit cards will undoubtedly continue, shaping the landscape of payments for years to come. Your thoughts matter! Drop a comment to help us improve. Thanks for reading!

This Article will answer your questions like:

The history of credit and debit cards dates back to the early 20th century, evolving from charge plates and metal cards used by affluent customers. The modern credit card emerged in the 1950s, notably with the Diners Club card, which allowed members to dine at various restaurants without cash. Debit cards gained popularity in the 1980s, allowing direct access to bank accounts for immediate transactions.

Credit cards began in the United States in the 1950s, with the Diners Club card being one of the first. Debit cards appeared in the late 1970s and gained traction in the 1980s, providing a convenient method for accessing funds directly from bank accounts. Both types of cards have revolutionized personal finance and consumer behavior.

Credit cards originated from the concept of charge accounts offered by merchants. In 1950, Diners Club issued the first true credit card, allowing customers to dine at various establishments. This model was quickly adopted by banks, leading to the creation of multiple credit card networks, enabling broader acceptance and the evolution of consumer credit.

The first credit card, the Diners Club card, was introduced in 1950 by Frank McNamara, allowing customers to pay for meals at participating restaurants without cash. This innovation laid the groundwork for modern credit cards, enabling transactions based on trust and future payment, and quickly gained popularity among consumers.

Debit cards first became available in the late 1970s, but their adoption surged in the 1980s with the introduction of electronic funds transfer systems. These cards allowed consumers to access their bank accounts directly for purchases, offering convenience and promoting a shift away from cash transactions in everyday shopping.

Diners Club significantly impacted credit card history by pioneering the concept of a multi-merchant charge card. Its introduction in 1950 marked the shift from store-specific charge accounts to universal credit. This model inspired banks to develop their credit cards, leading to the widespread adoption of credit cards we see today.

Bank of America created BankAmericard in 1958 to address consumer demand for a universal credit card. This initiative aimed to facilitate purchases across various merchants, enhancing customer convenience. The card’s success led to the establishment of Visa, significantly shaping the credit card industry and consumer finance.

Credit cards evolved significantly since their inception. Initially, they were simple charge cards for specific merchants. Over time, they adopted magnetic stripes, offering security and convenience. The introduction of rewards programs, contactless payments, and digital wallets further transformed the industry, enhancing customer engagement and security in transactions.

The first debit card was introduced in 1966 by Barclays in the UK. This card allowed customers to withdraw cash and make purchases directly from their bank accounts. It marked a shift towards electronic banking and paved the way for the widespread adoption of debit cards in subsequent decades.

Magnetic stripes, introduced in the 1970s, revolutionized credit card transactions by securely storing cardholder information. They enabled quick access to data during transactions, reducing processing time and errors. This technology laid the groundwork for the modern credit card system, enhancing both security and convenience for consumers and merchants.

Credit and debit cards gained worldwide popularity due to globalization, technological advancements, and changing consumer preferences. The rise of e-commerce, increased merchant acceptance, and the development of secure payment systems facilitated this growth. Additionally, promotional offers, rewards programs, and enhanced security features attracted consumers, making cards a preferred payment method.

Payment cards have evolved significantly since the early 20th century. Initially, charge plates were used by select consumers. The 1950s saw the introduction of credit cards, followed by the emergence of debit cards in the late 1970s. Innovations like magnetic stripes and EMV technology have continually enhanced security and usability, transforming how consumers conduct transactions globally.

First metal then paper, then plastic, then online, and then? both history and future of the credit cards is interesting.